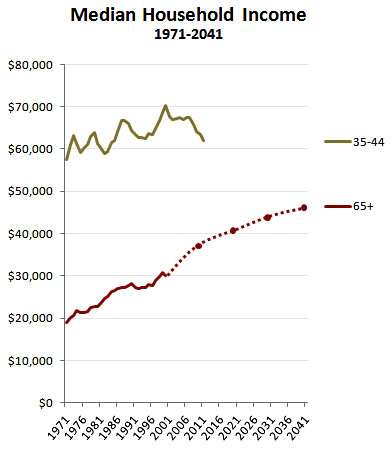

Our story so far: a few days ago I wrote a post describing the Social Security Administration’s MINT forecast of retiree income. As the chart on the right shows, they project that retiree income will continue its steady rise, increasing from $20,000 in 1970 to $46,000 in 2041 (adjusted for inflation). Based on this, I questioned whether the much-talked-about “retirement crisis” was for real.

Our story so far: a few days ago I wrote a post describing the Social Security Administration’s MINT forecast of retiree income. As the chart on the right shows, they project that retiree income will continue its steady rise, increasing from $20,000 in 1970 to $46,000 in 2041 (adjusted for inflation). Based on this, I questioned whether the much-talked-about “retirement crisis” was for real.

Dean Baker responded to my post, for which I’m grateful. He basically made five points:

- Social Security is a big part of the reason for rising retiree income. No argument there.

- Income replacement rates have declined from 95 percent for Depression-era workers to 84 percent for future retirees. This is true. However, as I explained on Friday, this is more because of sluggish income growth among workers than it is because retiree incomes are in any real trouble.

- 65-year-olds are living longer and are more likely to be working these days, which is part of the reason for strong incomes among seniors. Again, no argument there. But income is income, regardless of where it comes from. (It’s also worth noting that longer lifespans are primary a phenomenon of the well-off, not those with lower incomes.)

- Medicare premiums are increasing, which is an added expense for seniors.

- The MINT projections include imputed rent as part of income. In some cases this is fine, since living rent-free in a paid-off house does indeed have the same effect as cash income. In other cases, where retirees live in large houses with large imputed rents, it can give an inflated idea of how well off a retiree is.

The first three of these items don’t really change the picture. They’re just observations about the nature of the income that retirees are likely to have. Item #4 is relevant, but I think it’s cherry picking. Every age group has expenses that others don’t, and those expenses rise and fall differently. The only way to judge this fairly is to look at overall inflation rates for various age groups, and most efforts to do this have yielded only modest and ambiguous results. Finally, item #5 is a good point. It probably inflates the MINT projections modestly.

Overall, then, I don’t think this affects my point too much. If you revised the MINT projections to take into account CPI-E and made an adjustment for possible overestimates of imputed rent, the projected income line would probably go down a bit. But not very much. We’d still be looking at a world in which, relatively speaking, retirees are doing quite a bit better than current workers. In fact, their incomes are growing more strongly than pretty much any other age group.

This is why I’m not on board with calls to expand Social Security. Rhetoric and pretty charts aside, I simply don’t see any real evidence of a looming retirement crisis that urgently needs to be addressed, and I think focusing on it just distracts us from our real problem: sluggish wage growth among workers. And the funny thing is that Baker basically agrees:

Seniors income has been rising relative to the income of the typical working household because the typical working household is seeing their income redistributed to the Wall Street crew, CEOs, doctors and other members of the one percent….We can argue about whether young people or old people have a tougher time, but it’s clear that the division between winners and losers is not aged based, but rather class based.

That’s precisely right. I’m not willing to dismiss the relative problems of young and old quite as quickly—I think the young are being pretty badly screwed these days, and unlike seniors they have no one in Congress who really cares about them—but this is essentially a class problem, not an age problem. We should be doing everything possible to raise low and middle incomes regardless of age. If we do that, retirees will benefit, but so will everyone else.

This is obviously a lot harder than a simple crusade to expand Social Security. But the latter helps plenty of people who don’t really need it, while the former helps those who do. If part of helping those with low and middle incomes means changing Social Security payouts to reduce the future growth rates of high earners and increase the future growth rates of lower earners, that’s fine with me. But if I can borrow Baker’s headline, we need to keep our eye on the ball here. Let’s stop inventing crises that don’t really exist. If we want to move the Overton Window, let’s move it for the thing that really matters: the fact that the fruits of economic growth now accrue almost entirely to the rich, with the rest of us treading water at best. That’s the transcendent economic problem of the 21st century.